Euro Crisis and Impact on Global Financial Markets

May 27, 2010

By Padmini Arhant

It originated in Iceland with the pervasive subprime mortgage factor and similarly affected other economies like Ireland, Greece, Portugal and Spain, referenced as PIGS.

Although, every nation in this category share the contaminated ‘derivative’ traded internationally, the lack of deficit control with the national budget exceeding the GDP growth also contributed to the meltdown and subsequently reflected in the poor credit rating.

More prominently, Greece identified with:

“Goldman Sachs between the years 1998-2009 has been reported to systematically helped the Greek government to mask its national true debt facts.

In September 2009 though, Goldman Sachs among others, created a special Credit Default Swap (CDS) index for the cover of high-risk national debt of Greece. This led the interest-rates of Greek national bonds to a very high level, leading the Greek economy very close to bankruptcy in March 2010.”

The culmination of internal and external mismanagement primarily led the Mediterranean economy to the brink of collapse seeking bailout from the European Central Bank (ECB), EU and IMF.

European Union was challenged with a predicament in the Greece bailout to either ignore the problem or address it to avert the contagion in Europe.

Since Greece is an EU member using the reserve currency euro in the 16 of the 27 states representing the eurozone, the former alternative would have had serious ramifications.

Besides, the euro being the second most traded currency in the world after the U.S. dollar; it has multifaceted impact on the financial markets dealing with high volume trading especially in the futures exchange.

The industrialized and emerging economies are in a bind with the euro value reduction, due to the competitiveness expansion in export trade. For example, the export oriented Germany is at a competitive edge with the United States, Japan and China irrespective of Germany specializing in high end industrial and heavy machinery equipments.

Hence, the euro crisis upside is the European nations gaining export affordability.

Accordingly, the emerging economy and the major U.S. creditor China is concerned about the potential split in global market share and availing the opportunity to reject the U.S. request for currency (renminbi) value adjustment, which has been set below the market determination despite China’s extraordinary trade surplus.

China’s currency, renminbi (RMB) or yuan (CNY) has been withheld from floating as the international currency in the foreign exchange market to protect the status quo.

At the same time, the positive aspect of the dollar appreciation is omitted in the evaluation and that being the foreign investments in U.S. dollars particularly the Treasury bills held by China is strengthened in value and guarantee long term security in futures contract.

Financial stability measures adopted by EU, IMF and ECB with approximately one trillion dollars of which a conditional rescue loan worth $110 billion to Greece is approved to reverse the negatives in the financial markets reacting to the euro downslide from the unsustainable government debts and deficit level.

Had the eurozone requirement on its union members to keep deficits below 3 percent of GDP maintained, Greece and other struggling economies need not have been subject to harsh austerity strategies that has resulted in protest among the mainstream population in Greece and Ireland.

Regardless, the current global financial crisis calls for wasteful expenditure elimination and the national budget review to direct investments in high value returns.

Appropriate actions involving tax hikes and spending cuts are necessary to balance the budget.

However, spending cuts targeting the fundamental programs inevitably generating revenues through productive workforce and consumers is counteractive.

Restoring essential programs and services for the job creation and preservation, youth education, citizens’ health care, social security, safe and clean environment nurture healthy and middle class society to ease the burden on the top 1% or 10% wealthy taxpayers in different economies.

Most importantly, the defense budget consuming a significant proportion of taxpayer revenue in the prolonged wars could be divested to peaceful and profitable opportunities benefiting the citizens at the domestic and international front.

The ideal solution for the European Commission and the monetary union to avoid rising deficits in Europe without compromising the member states’ sovereignty in their national fiscal policy decisions would be to establish an independent, non-partisan committee by the states to examine the individual spending and tax plan, rather than the centralized monitoring or the neighboring authority verifying it.

Further, the constitutional amendment by Germany to contain the deficit to 0.35 percent of GDP by 2016 provided the higher deficit not attributed to GDP decline is a trendsetter in curbing the economic crisis.

In concurrence with the economic experts’ advice – The ECB expediting the credit approval on government bonds used as collateral upon qualifying the self-regulated constitutional limit on deficits is prudent in deterring broad speculative lending activities.

Alongside, the EU sweeping financial reform with tough standards against the hedge fund managers including the two proposals by German Parliament:

Global financial transaction tax and Financial activity tax focused on CEO’s Personal Income & Bonuses are effective steps with the exception of the global financial transaction tax because it is eventually transferred to the end-consumer and may not be a viable option for all participants.

Nevertheless, international agreement on financial regulation by G-20 and other nations is crucial in order to emerge from the existing crisis and prevent the future economic recession.

The systemic risk in the multi trillion dollars ‘derivatives,’ that caused the financial debacle in Europe, Middle East (Dubai), North America, Asia and elsewhere demands stringent policies and independent investigations on fraudulent ventures.

The financial overhaul passed by the U.S. Senate last week has been under scrutiny by analysts with mixed response and elaborated in the article titled:

“New Financial rules might not prevent next crisis – Associated Press, Sun May 23rd. 2010 at 3.55 PM EDT. Reported by Jacobs from New York and contributed by AP writer Jim Drinkard.”

Unequivocally, closing the loopholes as detailed in the cited article and other reports is paramount to establish a financial system free of K street influence.

The apparent revolving-door relationship between Wall Street and Capitol Hill in which employees and consultants have moved in and out of high level US Government positions, with the prevalent conflict of interest is a hindrance to any legislation.

Only the electorates with the voting power in a democracy can remove the persisting obstacles by rejecting the special interest representatives in politics against meaningful legislation.

People as the consumers, taxpayers and voters are the ultimate force in achieving the progress for common good.

Thank you.

Padmini Arhant

Globalization

October 16, 2008

By Padmini Arhant

The twenty first century paved way to a new era in trade and commerce.

In the economic sector, the twentieth century policies such as NAFTA, CAFTA, and MFN… implemented to benefit the trading nations.

The economic model carried out on trial and error basis with deficiencies within yielded the net outcome.

The long-term strategy was to promote mutual economic growth and development.

There are different views and opinions on these trade policies.

———————————————————————————————

Source: http://news.thomasnet.com/IMT/archives/2004/01/the_pros_and_co_1.html – Thank you.

The Pros and Cons of NAFTA

By Katrina C. Arabe -Thank you.

Here are both sides of this raging debate:

Supporters say:

? The accord has stimulated democratic reform and opened markets in Mexico.

? According to the Bush administration, the agreement has been “improving lives and reducing poverty in Mexico.”

? The administration also claims that NAFTA has led to income gains and tax cuts amounting to about $930 each year for the average U.S. household of four.

? Many of the 20 million new jobs the U.S. generated from 1993 to 2000 can be attributed to the free-trade bloc that NAFTA created, the administration continues.

And negatives such as the escalating U.S. trade deficit and three years of dwindling factory jobs should be pinned on feeble demand abroad and the U.S. recession, certainly not on NAFTA, the administration contends.

? NAFTA brought in a flood of foreign investment and contributed to a 24% rise in Mexico’s per capita income. “NAFTA gave us a big push,” Vicente Fox, President of Mexico, tells Business Week. “It gave us jobs. It gave us knowledge, experience, technological transfer.”

Detractors contend:

? The agreement has taken a toll on both U.S. and Mexican jobs, according to the Institute for Policy Studies (IPS). While real wages for Mexican manufacturing workers declined 13.5%, more than half a million U.S. employees have entered government retraining programs after their companies moved production south or north of the border, says IPS.

? NAFTA has wiped out Canadian social programs, purports IPS.

? The pact has also destroyed Mexico’s small farmers, says IPS, bringing in an influx of subsidized U.S. food imports. In fact, about 1.3 million farm jobs have been lost since 1993, indicates a recent report by the Carnegie Endowment for International Peace. “NAFTA has been a disaster for us,” remarks pig farmer Julian Aguilera to Business Week.

? The Carnegie report also concluded that the pact has generated few new jobs in Mexico and might only be credited for a “very small net gain” in jobs in the U.S.

? The new study also found that NAFTA has been ineffective in stemming the tide of illegal Mexican immigrants entering the U.S. to find jobs. In fact, according to most estimates, the number of Mexicans working illegally in the U.S. surged to 4.8 million in 2000, more than twice the 1990 total.

What’s the Verdict?

So is NAFTA a success or a failure? While its backers and bashers continue to take impassioned positions, many choose the middle ground. In a recent Business Week article, Jeffrey Garten writes,

“When it came to job generation vs. destruction in the U.S., NAFTA’s impact has been pretty much a wash.” And the Carnegie Endowment for International Peace comes to the same conclusion, calling the pact “neither the disaster its opponents predicted nor the savior hailed by supporters.”

————————————

The Pros and Cons of CAFTA –

Source: http://www.allbusiness.com/north-america/united-states-new-york/1057929-1.html

Thank you.

By Cantor, Martin – Thank you.

Publication: Long Island Business News

Now that the Central American Free Trade Agreement-Dominican Republic is law, the question that lingers is whether it benefits Long Islanders.

For certain, CAFTA benefited President George W. Bush and congressional Republicans, who are trying make the GOP the place for the growing and politically influential Hispanic community. This strategy has helped Bush with the regional Hispanic population, who believe that great economic and job growth will result from CAFTA.

There is no doubt that eliminating tariffs and removing trade barriers makes commerce efficient, less costly and more profitable while also bringing hope that the profits would result in better working conditions and higher worker wages. CAFTA will succeed for global businesses, many of which call Long Island home.

But it may not live up to the hype of creating jobs and safer workplaces.

For Hispanics, who are Long Island’s fastest growing minority group, the hope was that the savings generated from eliminating trade barriers would be reinvested in plant and equipment in their countries of birth. The belief was that this reinvestment would expand manufacturing capacity and create a demand for jobs, thus improving living standards for the families and friends left behind.

Supporters of CAFTA say jobs and higher wages would reduce the flow of the undocumented workers because there would be little reason to come to this region in search of better salaries. Additionally, since many of these individuals work on Long Island to send money back home, some of the wages earned on Long Island could now remain here and help the local economy.

However, the reality is that there’s skilled labor at lower costs in the Far East. All of those locations present stiff competition.

With Long Island’s growing Hispanic community becoming an important regional economic segment that desires goods from Central America, one benefit may be that regional Hispanic entrepreneurs can use free trade to import lower cost goods for this expanding consumer market.

This may be the lasting legacy of CAFTA. That the United States, Canada, Central America, Mexico and the Dominican Republic have united in a trading bloc offering Long Island and its Hispanic entrepreneurs an opportunity for new economic growth.

————————————

Source: http://www.fas.org/man/crs/92-094.htm#back – Vladimir N. Pregelj, Economics Division. –

CRS – Issue Brief – Thank you.

Most-Favored-Nation Status of the People’s Republic of China.

On May 31, 1996, President Clinton issued his determination to extend China’s waiver and most-favored-nation (MFN) status for another year; and, on June 21, 1996, he issued a determination renewing the trade agreement with China for another 3-year term (through January 31, 1998).

On June 27, 1996, the House failed to pass H.J.Res. 182, which would have disapproved the extension of China’s waiver and MFN status, thus allowing both to remain in force through July 2, 1997. The House did, however, adopt a resolution (H.Res. 461) calling on various committees to hold hearings and report out appropriate legislation to deal with China on a variety of issues, including trade, weapons proliferation, human rights, and military policy.

Effects of Withdrawing China’s MFN Status —

Termination of China’s MFN status would result in duty increases on about 95% of U.S. imports from China. The cost effect of the increases would vary among the various product groups, but would on the whole be substantial.

———————————–

Source: http://www.cyfuture.com/pro-and-cons-of-outsourcing.htm – Thank you.

Pro and Cons of Outsourcing

Outsourcing has many advantages but at the same time it has some disadvantages that cannot be ignored. So let us look at some outsourcing pros and cons.

Pros of Outsourcing

Outsourcing as a trend has come into major scrutiny by the workers and media alike in the developed countries.

But most economists are sure that this condition is just a temporary one and will die down as conditions develop and people start taking a mature outlook towards outsourcing.

The Outsourcing advantage lies in the fact that it helps companies cut costs and stay ahead in the competition.

Outsourcing also benefits the citizens in developed counties as it provides high quality products at a cheaper rate also with better customer service.

Advantages of Outsourcing

• Companies can save up on operational costs. In fact most companies can cut their operating costs to half by outsourcing

• Get access to cheaper and more efficient labor

• Cut up on labor training cost

• Get access to better technologies at a cheaper cost

• Increase productivity

• Concentrate on core competencies

Companies today want to make use of the outsourcing advantage in order to progress and stay abreast of the competition.

This is the reason why more and more companies irrespective of certain failures are entering the race of outsourcing.

Cons of Outsourcing

Outsourcing is seen by companies in developed countries and workers in developing countries as a boon. But is the situation really that green? Let us look at some disadvantage of outsourcing.

Disadvantages of Outsourcing

• The company that outsourcers can get into serious trouble if the service provider refuses to provide business due to bankruptcy, lack of funds, labor etc

• Outsourcing requires the control of the process being outsourced by transferred to the service provider. Thus the company may loose control over its process

• The service provider in developing countries generally services many companies. So there are many chances of partiality owing to more payment by other parties

• The current employees in the company that outsourcers may feel threat due to outsourcing and may not work properly

• The attitude of people in the developed countries against companies that outsource is generally bad

These disadvantages are the reasons why companies should think twice before outsourcing.

Companies should adopt a planned approach towards outsourcing taking into account the interests of employees and customers alike and come up with a balanced advance.

Outsourcing services simply to beat competition or to follow your competitors can lead to problems in the future.

—————————————–

Source:http://econpapers.repec.org/article/eeejpolmo/v_3A30_3Ay_3A2008_3Ai_3A5_3Ap_3A725-735.htm

GLOBALIZATION AND INCOME INEQUALITY: IMPLICATIONS FOR INTELLECTUAL PROPERTY RIGHTS

Samuel Adams – Thank you.

Journal of Policy Modeling, 2008, vol. 30, issue 5, pages 725-735

Abstract: This paper examines the impact of globalization on income inequality for a cross-section of 62 developing countries over a period of 17 years (1985-2001).

The results of the study indicate that globalization explains only 15% of the variance in income inequality.

More specifically, the results show that (1) strengthening intellectual property rights and openness are positively correlated with income inequality; (2) foreign direct investment is negative and significantly correlated with income inequality but this is not robust to different model specifications; (3) the institutional infrastructure is negatively correlated with income inequality.

The study’s findings and the review of the literature suggest that globalization has both costs and benefits and that the opportunity for economic gains can be best realized within an environment that supports and promotes sound and credible government institutions, education and technological development.

———————————————————————————————–

Review and Analysis: By Padmini Arhant

The current unemployment rate in the United States is 6.1 percent.

All of the above factors combined with the serious financial crises contribute to the decline in the job market.

The current Stock Market volatility is a reaction to the multifaceted problems surrounding the economic infrastructure.

With the interventional policies by the governments and the monetary authorities worldwide, the U.S. and global markets should stabilize slowly but steadily.

Meanwhile, the equity and liquidity markets with cash and lending instruments should facilitate the required rebound in the market.

It was determined that the credit markets’ resistance is from the weak sales projection by the Retail industry, which is related to reduced consumer spending resulting from high unemployment rate.

It is imperative for the business groups to focus on the employment situation now, hurting their operation and survival in the global economy. The depletion of capital resources and credit crunch is one of the factors for the massive layoffs at present.

Restoration of American jobs is paramount to the revival of the U.S economy.

The stabilizing of the U.S. economy will boost market confidence and the performance level.

This would also contribute to the strengthening of the U.S. dollar much required to offset Trade deficits.

The Corporations and the governments must coordinate their efforts to review,

1. Policies like NAFTA, CAFTA, MFN, Outsourcing … with fundamental flaws and reestablish a renewed structure to benefit the American workforce and the international competitive labor.

2. Renegotiate treaties and agreements with WTO members and other agencies…ILO at home and overseas to redesign models with fair trade policies, employment practices and environment laws.

3. Prioritize and protect American jobs and labor laws over shareholders interests and corporate profits. By doing so, the increased productivity would yield the desired stock value for the Corporations.

4. International labor force is equally important in the equation. Appropriate measures … required to curb the exploitation of cheap labor in poorer and under developed nations by the multinational corporations.

5. The developing nations currently benefiting from U.S corporate investments through outsourcing should reciprocate with return investments on U.S. goods and services. The general options are to purchase high-end products and engage U.S. companies for infrastructure projects.

The concern for the loss of American jobs is legitimate. Any frustration and anxiety by the American work force is also normal.

Since, U.S. economy is the foundation of the global economy; idle American work force is counter-productive for Corporations shipping jobs overseas in pursuit of market share of the emerging economies.

The sluggish U.S. economy will not serve well for the global economies dependent on U.S. trade.

On another serious note, the print press and media have an ethical and moral responsibility to portray the global economic environment and the activities in a fair and responsible manner.

Any rhetoric diminishing the economic progress/status and professional talent of other nations such as the one recently cited by the researcher specializing in globalization in San Jose Mercury News article, will hinder the new world order effort — aimed at providing prosperity for all.

Ironically, both the news organization and the consultants fail to identify the real beneficiary i.e. the Corporations in the outsourcing deals and other trade policies.

It would be more appropriate for these individuals to be part of the solutions rather than a problem.

Inevitably, U.S. prosperity is vital for global progress.

Thank you.

Padmini Arhant

Stock Market Performance

October 14, 2008

The Stock Market came roaring back on October 13, 2008 and was a major cause for celebration across the globe.

The collective and collaborative effort by the “Heads of Government” through G7 and G20 meetings, in coordination with the global monetary authorities like the World Bank and the International Monetary Fund yielded the much-required morale boost in the financial markets. Their immediate action to respond to the crisis is praiseworthy.

Despite the consolidated action to jumpstart the markets, the stock market is struggling to sustain the momentum gained on the previous day. Obviously, the indication is that the measures in the past hours and days to guarantee the smooth functioning of the financial system is not adequate.

A selective opinion highlighting the reasons for the problems currently experienced in the credit markets –

Source – http://www.americaneconomicalert.org – Thank you.

Why Federal Reserve Policy is Failing

Monday, October 06, 2008

Commentary by Thomas I. Paley, Ph.D.

The Federal Reserve and U.S. Treasury continue to fail in their attempts to stabilize the U.S. financial system. That is due to failure to grasp the nature of the problem, which concerns the parallel banking system. Rescue policy remains stuck in the past, focused on the traditional banking system while ignoring the parallel unregulated system that was permitted to develop over the past twenty-five years.

This parallel banking system financed vast amounts of real estate lending and consumer borrowing. The system (which included the likes of Thornburg Mortgage, Bear Stearns and Lehman Brothers) made loans but had no deposit base. Instead, it relied on roll-over funding obtained through money markets. Additionally, it operated with little capital and extremely high leverage ratios, which was critical to its tremendous profitability. Finally, loans were often securitized and traded among financial firms.

This business model has now proven extremely fragile. First, the model created a fundamental maturity mismatch, whereby loans were of a long term nature but funding was short-term. That left firms vulnerable to disruptions of money market funding, as has now occurred.

Second, securitization converted loans into financial instruments that could be priced according to market conditions. That was fine when prices were rising, but when they started falling firms had to take large mark-to-market losses. Given their low capital ratios, those losses quickly wiped out firms’ capital bases, thereby freezing roll-over funding.

In effect, the parallel banking business model completely lacked shock absorbers, and it has now imploded in a vicious cycle. Lack of roll-over financing has compelled asset sales, which has driven down prices. That has further eroded capital, triggering margin calls that have caused more asset sales and even lower prices, making financing impossible for even the best firms.

Though the parallel banking system engaged in riskier lending than the traditional banking system, those differences were a matter of degree. Traditional banks like Washington Mutual, Wachovia, and Citigroup have also all lost huge sums. However, the traditional banking system is more protected for two reasons.

First, traditional banks are significantly funded by customer deposits. Ironically, such deposits can be withdrawn on demand and are in principle even more insecure than short term roll-over funding. However, they stay in place because of federally provided deposit insurance.

Second, traditional banks are significantly shielded from mark-to-market accounting because they hold on to many of their loans. These loans are therefore priced by auditors on a mark-to-realization basis. However, if they were securitized their market value would be significantly lower owing to current disruptive market conditions.

The bottom line is that the banking system is in better shape not because of its virtues, but because of policy. Deposit funding is safe because of deposit insurance. Banks are spared mark-to market losses because of different accounting rules. And the Federal Reserve is providing banks with massive liquidity infusions through its discount window and its various emergency auction facilities.

Policy has therefore ring-fenced traditional banks. But in the meantime it has left the parallel system in the cold, leaving a gaping hole in the policy dyke.

This policy stance reflects the Fed’s continuing attachment to an antiquated view of the system whereby it takes responsibility for traditional banks and nothing else. Such a policy makes no sense and will fail. The Fed encouraged development of the parallel system, and that system undertakes many of the same activities as traditional banks. Meanwhile, failure of the parallel banking system will continue putting downward pressure on asset prices and lender confidence.

The Treasury’s proposed seven hundred billion dollar asset purchase program will help put a needed floor under asset prices. However, it does nothing to tackle the parallel banking system’s roll-over funding crisis that is crimping lending and pushing firms into bankruptcy. That is causing distress to spread far beyond the mortgage market, undermining the ability of any asset purchase program to put a floor under asset prices.

The urgent implication is the Fed (and other central banks) must extend its safety network to include the parallel banking system. Just as the traditional banking system needs liquidity assistance, so too does the parallel system. That assistance can be provided through such vehicles as the discount window and Federal Reserve auction facilities, and it should be allocated to qualified firms able to post appropriate collateral.

A credit based system is a chain, and a chain is only as strong as its weakest link. The Federal Reserve’s antiquated view has it protecting links connected to the traditional banking system while neglecting everything else. That is a recipe for failure.

Dr. Thomas Palley is a widely published economist and was formerly Chief Economist at the US-China Economic and Security Review Commission.

____________________________

Analysis: Certainly, the emphasis is on the oversight with effective policies for the entire financial structure to alleviate stagnation in the liquidity markets. The investor confidence overall is marred with concerns and skepticism despite stunning performance on October 13, 2008.

The resistance from the free market system towards proposed measures is one of the factors for the current trend. However, the necessary action could eliminate many underlying problems surrounding the entire financial infrastructure, contributing to the volatility in the markets.

Meanwhile, the investors’ active participation to restore momentum and strengthening market gains across all sectors is important for the common good and benefit in the short and long run.

An optimistic approach to the crisis with an absolute integrity in the implementation of policies will assist the markets to rebound now and in the future.

Thank you.

Padmini Arhant

My Life – Autobiography by Padmini Achintya Arhant

Upcoming Podcasts and Website Accessibility – Padmini Arhant

OM Nama Sivaya – Glory to Almighty God!

OM Nama Sivaya - Glory to Almighty God !

Traditions from Abroad – Men in Tradition

EVIl invites PERIL

Happy Pongal! Happy Makara Sankaranthi! 2025

Happy Pongal!

2025

Padmini Arhant

Image Credit: Artist via paid subscription source. Thank you.

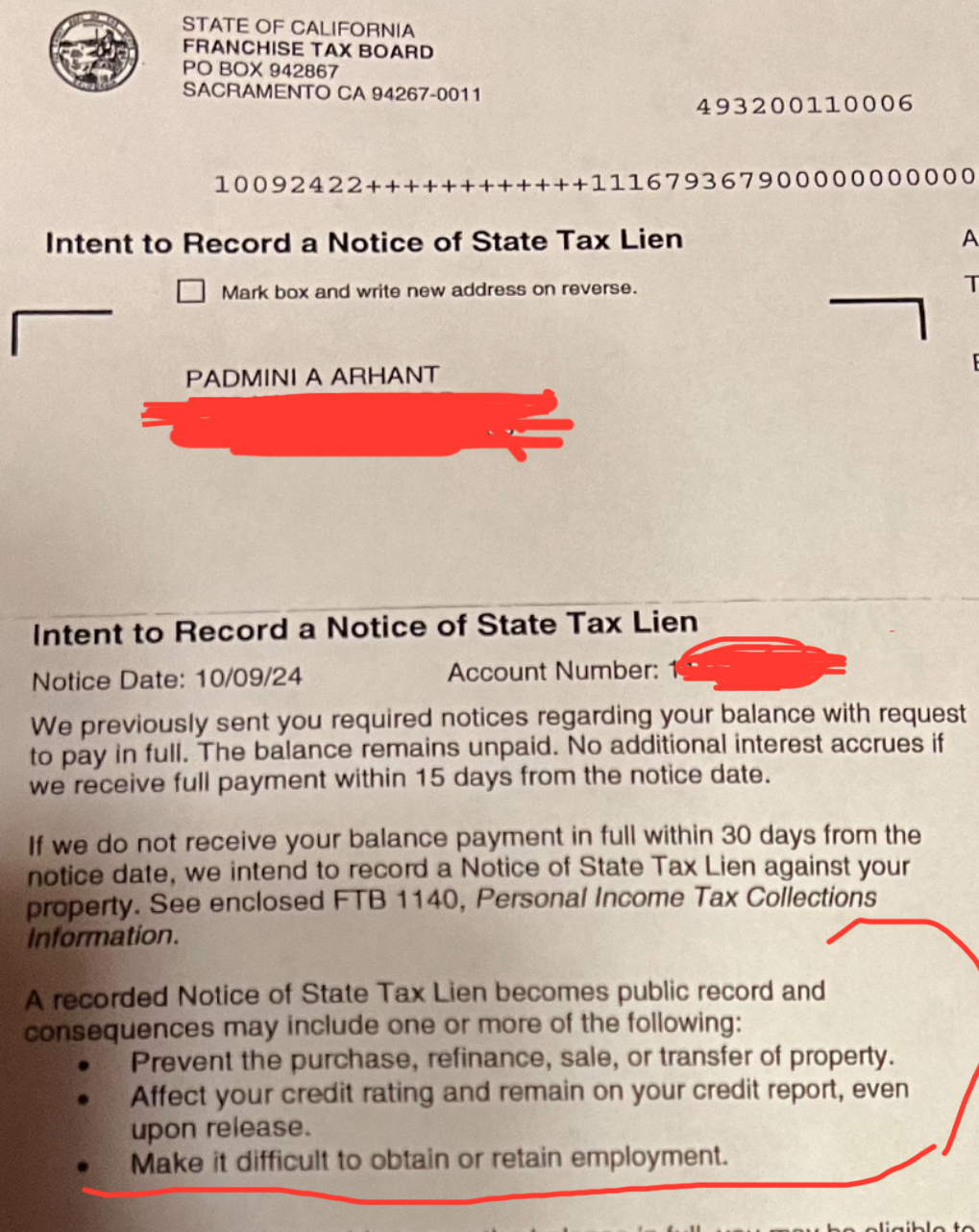

FASCISM WRIT LARGE AS THE SO-CALLED DEMOCRAT

FYI : California Franchise Tax Board

Sacramento, CA

For the umpteenth time – Please refer to the third letter dated June 13, 2024 received by you with signed delivery confirmation. The letter with proof of tax payment on August 23, 2023 with 2022 tax return e-filing, bank confirmation on the payment and email references were all enclosed for your reference and settlement on this matter.

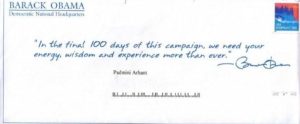

Yet, for political reasons the weaponization of taxpayer funded State and federal departments and agencies trending since 2009 – 2016 against then Republican Tea Party by Barack Obama in personal vendetta against them for questioning Barry Soetoro’s birth certificate was responded with terminating the Republican Tea Party in the first term in 2012. It was just the tip of the iceberg.

The trend then continued against political opponent Donald Trump from impeachment proceedings to libel suits with no end in sight.

Similar tactics deployed against me and my family by the same members i. e. The OBAMAS having abused and continue to use and abuse our presence, profile and all things politically and personally exclusively beneficial to them from DAY ONE until now by tagging, trolling, pirating anything positive and impressive for image enhancement despite being warned to cease and desist.

Notwithstanding thousands of $$$ fraudulently amassed from us by the fleecing scammers, abusers and parasitic exploiters till date make them indebted to me personally and my family.

Politics’ underhanded bullying and harassment is sheer desperation in the face of own extinction.

If you can’t express gratitude as the chief beneficiaries of our timeless sacrifice and benevolence, the least you could do is abandon the self-destructive attitude hurting you in the attempt to harm others.

By the way – nothing to do with Angel Reese and anyone with Brown last name in your nuanced attacks directed at me. They are all yours and you can keep them.

That goes for Kamala Harris – the name Kamala adopted from my explanation of my first name conveniently plagiarized for political and fortune harvesting in your end game once again for en masse deception like in 2009 – 2016.

The same resumed in 2021 – 2024 with blatant intention to extend the sham indefinitely with ludicrous WOKISM.

Originality and FAKE distinction is authenticity never in requirement to be anything other than true self unlike the impostor ever remaining fraudsters in vain.

Padmini Arhant

Character Not Color That Ever Matters

Lord Ram emphasized on deeds aka Karma not creed that matter in living and after life.Dr. King – related to that by echoing the content of the character not color that matters.

It’s time to move towards clear aka colorless society and nurture the importance of deeds with merit and virtues instead of remaining stuck in color coding society. Such trend only reveal opportunism with polarization rather than unity and harmony amongst human race.

Padmini Arhant

Exploitation – Knows Nothing About Gratitude and Truthfulness

Padmini Arhant – Gaza War and Rafah Air Strike

Padmini Arhant – PadminiArhant.online

Independent Free Palestine – Jan 2024 Speech

Celebration – Bright, Beautiful & Picturesque

Bright, Beautiful & Picturesque

Swastika – The Sacred Symbol – All is Well

Organic Intelligence Erring!

The ones flaunting the so-called organic intelligence with constant jibes at the allegedly artificial intelligence could perhaps seek assistance from the latter in spelling adjectives correctly to make sense of the message. Even basic spell check feature would serve the requirement.

The country is indeed precious not prescious than any individual, entity, political party, institution and organization.

Needless to say, it is applicable all around without exception.

Unlike the trend, smothered in hypocrisy beckoning others to do what is apparently unacceptable to selves to the extent of blasphemy.

Padmini Arhant

Get over the 🤚🏽✋✌🏼✌️✌🏿 🙏🏽🙏🏻🙏🏽🙏🙏🏿 mania!

Get over the mania!

🙏🏽🙏🏻🙏🏽🙏🙏🏿

mania as that is not going to deliver what is aimed at and desired in vain except confirming your asinine indulgence.

mania as that is not going to deliver what is aimed at and desired in vain except confirming your asinine indulgence.Besides in politics such as Indian corrupt criminal signature trait is exclusively yours and no monkey see monkey do act can change it for it is attached to you like skin and bone.

Padmini Arhant

Padmini Arhant with Divinity Shiva

Celebration of Lord Krishna

Message to Humanity – Padmini Arhant

Spread peace and engage in non-violence. Speak truth with courage. Heed your conscience. Respect life. Serve your nation and people with honesty and integrity. Espouse human values and exemplify in deeds with care and compassion. Voice concern over injustice. Be part of the solution and not the problem. Love mankind and environment for universal harmony.

Peace is Eternal Bliss.Padmini Arhant

தமிழ் புத்தாண்டு 2022 நல் வாழ்த்துக்கள்! Tamil New Year 2022 Greetings!

Padmini Arhant and Roshni Greeted by the Brilliant Light in the Horizon

Words of Wisdom from Venerable Gautam Buddha

Words of Wisdom from Venerable Gautam Buddha

Tamil OM Symbol & Pranava Manthiram

Absolute Truth

Reunion with Divinity God Shiva at Holy Mt.Kailash 2019

Padmini Arhant interaction with God Shiva during Parikrama of Mt.Kailash

Padmini Arhant Kailash Lake Manasarovar Pilgrimage 2019

Padmini Arhant on Parikrama or Circumambulation of Mt. Kailash

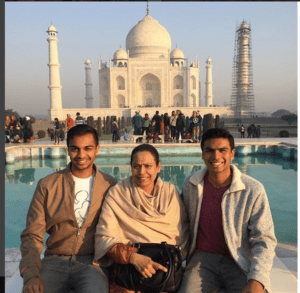

ARHANT Family at Famous Taj Mahal

Gautam Buddha’s Words of Wisdom

Peace Pledge